The U.S. LNG Pause: Implications for the Global Fertiliser and Food Markets

Peter Fawley

The U.S. LNG Pause

On January 26, the Biden administration announced a temporary pause on approvals of new liquified natural gas (LNG) export projects. The pause applies to proposed or future projects that have not yet received authorisation from the United States (U.S.) Department of Energy (DOE) to export LNG to countries that do not have a free trade agreement (FTA) with the United States. This is significant as many of the largest importers of U.S. LNG–including members of the European Union, the United Kingdom, Japan, and China–do not have FTAs with the United States. Without the DOE authorisation, an LNG project will not be allowed to export to these countries. The policy will not affect existing export projects or those currently under construction. The Department of Energy has not offered any indication for how long the pause will be in effect.

This pause will have political and economic implications across the globe, and is expected to apply further pressure to the LNG market, fertiliser prices, and agricultural production. The following analysis will first delve into the rationale for the pause, the expected impact it will have on global LNG supplies, and the associated risks this poses for the fertiliser and food markets. It will then examine the impact of this policy change on India’s agricultural sector, given that the country is heavily reliant on LNG imports to manufacture fertilisers for agricultural production. The article will conclude with brief remarks about the pause.

Reasons for the Pause

According to the Biden administration, the current review framework is outdated and does not properly account for the contemporary LNG market. The White House’s announcement cited issues related to the consideration of energy costs and environmental impacts. The pause will allow DOE to update the underlying analysis and review process for LNG export authorisations to ensure that they more adequately account for current considerations and are aligned with the public interest.

There are also likely political motivations at play, given the upcoming election in the United States. Both climate considerations and domestic energy prices are expected to garner significant attention during the lead up to the 2024 U.S. presidential election. The Biden administration has been under increasing pressure from environmental activists, the political left, and domestic industry regarding the U.S. LNG industry’s impact on climate goals and domestic energy prices. In fact, over 60 U.S policymakers recently sent a letter to DOE urging its leadership to reexamine how it factors in public interests when authorising new licences for LNG export projects.

These groups have argued that the stark increase in recent U.S. LNG exports is incompatible with U.S. climate commitments and policy objectives, as the LNG value chain has a sizeable emissions footprint. Moreover, there is a concern about the standard it sets for future policy. An implicit and uncontested acceptance of LNG could signal that the U.S is wholly committed to continued use of fossil fuels as an energy source, leading to more industry investments in fossil fuels at the expense of renewable energy technologies. In an unusual political alliance, large U.S. industrial manufacturers are lobbying alongside environmentalists to curb LNG exports. These consumers, who are dependent on natural gas for their manufacturing processes, worry that additional LNG export projects will raise domestic natural gas prices. Therefore, the pause may then be interpreted as an acknowledgement of these concerns and an attempt to reassure supporters that the Biden administration is committed to furthering its climate goals and securing lower domestic energy prices.

Impact on LNG Supplies

Since the pause only pertains to prospective projects, there will be no impact on current U.S. LNG export capacity. However, the pause may constrain supply and reduce forecasted global output as the new policy indefinitely halts progress on proposed LNG projects that are currently awaiting DOE authorisation. In the long-term, this announcement has the potential to tighten the LNG market, potentially resulting in increased natural gas prices and other commercial ramifications. Because the U.S. is currently the world’s largest LNG exporter, a drop in expected future U.S. supplies may force LNG importers to seek to diversify their supply. Some LNG buyers will likely redirect their attention to other, more certain sources of LNG, such as Qatar or Australia. Additionally, industry may be more keen to invest in projects in countries that have less regulatory ambiguity related to LNG projects.

Risk for the Global Fertiliser and Food Markets

Natural gas is key to the production of nitrogen-based fertilisers, which are the most common fertilisers on the market. With regard to the use of natural gas in fertiliser production, most of it (approximately 80 per cent) is employed as a raw material feedstock, while the remaining amount is used to power the synthesis process. Farmers and industry prefer natural gas as a feedstock as it enables the efficient production of effective fertilisers at the least cost.

The U.S. pause on new LNG projects is an unsettling signal to already fragile natural gas markets given the existence of relatively tight current supplies and a forecasted shortfall in future supply levels. This announcement will exacerbate vulnerabilities and put increased pressure on global supplies, potentially leading to greater volatility and price escalation. Additionally, increased global demand for natural gas will further strain the LNG market. Therefore, global fertiliser prices may increase given that natural gas is an integral input in fertiliser production. Natural gas supply uncertainty stemming from the U.S. announcement may not only impact market prices for fertiliser, but could also increase government subsidies needed to support the agricultural industry to protect farmers from price volatility. Due to the increased subsidy outlay, government expenditure on other publicly-funded programs could plausibly be reduced.

The last time there was a significant shock to the natural gas market, fertiliser shortages and greater food insecurity ensued. Following the 2022 Russian invasion of Ukraine, there was a stark increase in natural gas prices, which led to a rise in the cost of fertiliser production. This prompted many firms to curtail output, causing fertiliser prices to soar to multi-year highs. Higher fertiliser costs will theoretically induce farmers to switch from nitrogen-dependent crops (e.g., corn and wheat) to less fertiliser-intensive crops or decrease their overall usage of fertilisers, both of which may jeopardise overall agricultural yield. Given that fertiliser usage and agricultural output are positively correlated, surging fertiliser costs in 2022 translated into higher food prices across the world. While inflationary pressures have subsided in recent time, global food markets remain vulnerable to fertiliser prices and associated supply shocks. This is especially true for countries that are largely dependent on their agricultural industry for both economic output and domestic consumption. Food insecurity and global food supplies may also be further constrained by unrelated impacts on crop yields, such as extreme weather and droughts.

Case Study: India

The future LNG supply shortfall and its impact on fertiliser and food markets may be felt most acutely by India. The country is considered an agrarian economy, as many of its citizens – particularly the rural populations – depend on domestic agricultural production for income and food supplies. Fertiliser use is rampant in India and the country’s agricultural industry relies heavily on nitrogen-based fertilisers for agricultural production. With a steadily rising population and a finite amount of arable land, expanded fertiliser usage will be necessary to increase crop production per acre. As a majority of India’s fertiliser is synthesised from imported LNG, the expected increased demand for fertiliser will necessitate more LNG imports.

LNG imports to India are projected to significantly rise in 2024, with analysts forecasting a year-on-year growth of approximately 10 per cent. Over the long-term, the U.S. Energy Information Administration predicts that overall natural gas imports to India will grow from 3.6 billion cubic feet per day (Bcf/d) in 2022 to 13.7 Bcf/d in 2050, a 4.9 per cent average annual increase. The agricultural industry is a substantial contributor to this growth. This trend is only expected to continue, as India has announced that it plans to phase out urea (a nitrogenous fertiliser) imports by 2025 in order to further develop its domestic fertiliser industry. To ensure adequate supplies for domestic urea production, India is expected to increase its natural gas demand and associated reliance on LNG imports. A recent agreement between Deepak Fertilisers, a large Indian fertiliser firm, and multinational energy company Equinor exemplifies this. The agreement secures supplies of LNG (0.65 million tons annually) for 15 years, starting in 2026.

Concluding Remarks

The U.S. pause on new LNG export facilities will have ramifications for the global natural gas market and supply chain. While current export capacity will not be jeopardised, the policy change will delay future projects and may put investment plans into question. The pause will also have implications for downstream markets in which natural gas is an important input, such as the fertiliser market. There are a couple of questions that now loom over the LNG industry: (1) what will be the duration of the pause; and (2) to what extent will the pause affect LNG markets?

While the U.S. Department of Energy has given no firm timeline for the pause, analysts estimate – based on previous updates – that the DOE review will likely last through at least the end of 2024. The expectation is that the longer the pause remains in effect, the more uncertainty it will create, especially as it relates to private industry investment decisions and confidence in U.S. LNG in the long-term. In addition to the fertiliser and food markets, transportation, electricity generation, chemical, ceramic, textile, and metallurgical industries may all be affected by the pause. One potentially positive consequence is that because LNG is often thought of as a transitional fuel (between coal and renewable energies), a large enough impact on LNG supplies could accelerate the energy transition directly from coal to renewable sources of energy, providing a boost to the clean energy technologies market. However, the pause may also create tensions with trading partners as it could be interpreted as an export control or a discriminatory trade practice, both of which stand in violation of the principles of the multilateral rules-based trading system. This may expose the U.S. to potential challenges and disputes at the World Trade Organization. Although it may be some time before we are provided concrete answers to these questions, the results of the 2024 U.S. presidential election will provide some insight into what LNG policies in the U.S. will look like going forward.

2024 Elections Report: Risks & Opportunities for Commodities Sector

In the ever-evolving landscape of global commodities, the year 2024 stands as a pivotal juncture marked by transformative elections across diverse regions. As nations prepare to cast their ballots, the outcomes hold the power to shape policies and strategies that will significantly influence energy, trade relations, and resource management worldwide.

This report encapsulates the intricate intersections between political shifts and their repercussions on the commodities sector. London Politica’s Global Commodities Watch has made a selection of the most significant countries, and analysed the potential impact of elections based on election programmes, past policies, and scenario planning.

India’s Rice Export Ban: International Responsibility and the Climate Crisis

On the 20th of July 2023, the Government of India took a significant step to address its domestic food security concerns by imposing a prohibition on the export of non-Basmati white rice, including both semi and wholly-milled varieties. This assertive play comes amidst a pressing need to ensure an adequate food supply within the nation.

Source: Statista

A press release from the Ministry of Consumer Affairs states that it was implemented to “ensure adequate availability” and “allay the rise in prices in the domestic market.” The late arrival of monsoon rains forecasted a potential shortage. Since then, however, there have been heavy showers leading to extreme flooding in key rice-growing areas in North India, ultimately destroying crop output. This has translated to a 14-15% domestic price rise of rice in the month of March itself. Furthermore, its stock-to-use ratio (a standardised ratio that measures stocks and gives insight into food security) will drop to its lowest point in 5 years. Combined with the high price of tomatoes (increased 340% year-to-date), the harsh reality of food insecurity has started to set in. The export ban is supposedly a strategic endeavour to showcase the current Prime Minister, Mr Modi’s prioritisation of food security before the upcoming union elections in 2024. This move can be woven into the rise of resource nationalism, examined more closely by Danial Ahmed in a previous report, where he points towards the possible movement to soft commodities. In this context, Reuters has reported that contracts worth an estimated $1 billion could be at risk, indicating the certainty of this shift.

Source: The Hindu

With the already fragile global food market struggling through the repercussions of the ongoing crisis in Ukraine, analysts are concerned about the anticipated impact of this ban. India is the largest rice exporter globally, accounting for a staggering 40% of the rice trade with exports totalling 22.2 million tons. The country’s rice exports also surpass the combined total of the next four largest rice-exporting nations, which will not be able to meet the supply deficit from this ban, exacerbating the existing global food shortage crisis and putting additional pressure on food prices worldwide.

While the ongoing conflict in Ukraine disrupts agricultural production and exports, recently seen with Russia backing out of the UN brokered Black Seas grain deal, the sudden spike in basmati rice demand adds another layer of complexity to the global food insecurity puzzle. Furthermore, China, the largest rice producer in the world, but also the biggest grain importer, has had an abysmal monsoon with its soil moisture levels of the rice growing regions at a very low level, which will lead them to demand more rice for import due to a domestic shortage. This is due to the El Nino Phenomenon, which describes unusually warm waters in the Pacific Ocean impacting wind movement and therefore rainfall and will have more significant effects in the coming months. The amalgamation of geopolitical tensions and climate-induced agricultural crises poses a grave threat to food availability and affordability worldwide.

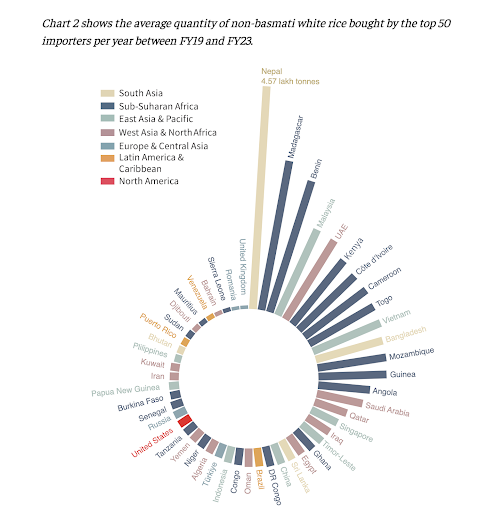

India’s rice ban also unequally targets the most vulnerable with top importers of Indian non-basmati rice including Benin, Bangladesh, Angola, Cameroon, Djibouti, Guinea, Ivory Coast, Kenya, and Nepal: all developing nations with poor historical food security trends. Considering historical evidence of India’s ban on wheat export and the wording of the notification, it might still continue to allow the sale of non-basmati rice to its neighbours. In this case, the market impact may be limited. However, considering the current government’s hardline posture, a hard ban with large implications for dependent countries is a possibility.

Source: The Hindu

That said, developed countries do not have it easy either; the large Indian diaspora (close to 18 million people) is allegedly panic buying Basmati rice as well, further deepening disparities in the global food shortage. In the United States especially, posts on Twitter(X) have shown large crowds and empty rice shelves, with some stores implementing a ‘Only 1 rice bag per family’ policy. This has exponentially increased Basmati rice prices in the US with a 9kg bag of rice selling at $27. The community fears a potential ban on Basmati Rice as well.

However, Asian Rice Exporting Nations have been able to profit from this supply deficit; Thailand and Vietnam have both experienced a 5% rise in price since the ban. The price of Vietnam’s rice has surpassed its highest level since 2011 and Thailand’s is at a 2-year high.

In conclusion, India's decision to impose a ban on the export of non-Basmati white rice marks a significant move with far-reaching implications. Driven by the urgency to secure its domestic food security needs, the government's action reflects its commitment to prioritising the well-being of its citizens amidst the challenges posed by climate-induced crises. It truly shows how in today’s world, all politics are climate politics

India's Growing Reliance on Russian Oil Imports

Since Russia's full-scale invasion of Ukraine in 2022, India’s reliance on Russian crude oil has increased tenfold. The proportion has risen from as little as 2% of total crude imports in 2021/2022, to 20% in June 2023. Recent estimates suggest that this percentage may reach as high as 30% by the end of the year.

In the wake of the invasion, there has been a largely concerted effort to sanction Russia’s economy and prevent it from further funding their war of aggression. A key component of the sanctions have been directed at Russia’s oil industry, Russia being the world's third largest producer and second largest crude oil exporter.

In December 2022, the EU’s sixth sanctions package came into effect, banning seaborne crude oil and petroleum products from Russia (90% of total oil imports from Russia). This move complimented similar bans enforced in the USA and the UK. Yet an additional component of the combined sanctions effort has been a price cap on Russian crude oil, which set the maximum price at $60 per barrel of crude. Despite the fact that the G7 countries (USA, UK, France, Germany, Italy, Japan, Canada and the EU) have already agreed to ban or phase out Russian crude imports, the cap has given leverage to uninvolved countries, including India, when negotiating prices with Russia.

The rapid increase in Indian imports from Russia suggests that India has been able to harness Russia’s weakened bargaining position. At the same time this new arrangement has put downward pressure on the oil prices charged India’s former suppliers in OPEC, primarily, Iraq and Saudi Arabia

Source: Reuters

The price differential between Russian and OPEC sourced crude, provides a clear basis in explaining India’s shift. Taking the April 2023 price as a point of comparison, India was able to pay as little as $68 per barrel for Russian imported oil, while oil from Iraq (traditionally India’s largest supplier) was priced at $77 per barrel and oil from Saudi Arabia cost as much as $86 per barrel. During the month of April, the overall OPEC basket price ranged from $79 to $86 per barrel. The price gap between OPEC suppliers and Russia makes a clear case for India’s growing imports from Russia, while the significantly lower price of Russian crude demonstrates the impact of the $60 price cap.

Source: Euronews

The challenges posed by India’s growing taste for Russian oil are twofold. In the first instance, while the price of Russian oil is considerably lower than OPEC in this case, the $68 per barrel price tag is still well over the imposed price cap, revealing the limitations of the price cap regime. In the second instance, India has become a rapidly growing market for Russian oil and as such a prop for the Russian war economy. While EU oil imports declined, figure 2 shows the relative increase of Indian oil imports, partially offsetting the impact of oil sanctions. India’s growing reliance on imported Russian oil has already become a point of contention with Western leaders. With the forecasted increase of India’s Russian oil imports, it is likely to remain so.

Image credit: President of Russia via Wikimedia Commons