A Strait Betwixt Two

As the Yemeni Houthi group's assault on maritime vessels continues to escalate, the risk to key commodity supply chains raises global concern. As analysed in this series' previous article (available here), conflict escalation impacts the region's security, impacting key trade routes and global trade patterns. The Suez Canal is a key trade route whose stability and security could impact and shift trade dynamics. As the search for alternative trade routes ensues, the Strait of Hormuz makes use of a power vacuum to expand its influence.

Suez Canal

The Suez Canal is a 193-kilometre waterway that connects the Red Sea to the Mediterranean Sea. Approximately 12% of global trade passes through the Canal, granting it vast economic, strategic, and geopolitical influence on a global scale. This canal shortens maritime trade routes between Asia and Europe by approximately 6,000 km by removing the need to export around the Cape of Good Hope and serves as a vital passage for oil shipments from the Persian Gulf to the West. Approximately 5.5 million barrels of oil a day pass through the Canal, making it a ‘competitor’ of the Strait of Hormuz.

Global trade via the Suez Canal is likely to decrease as a result of the rising tensions near the Bab el-Mandeb Strait. Due to their geographic predispositions, the Bab el-Mandeb Strait and the Suez Canal are interdependent; bottlenecks in either trade choke point will have a knock-on effect on the other. Bottlenecks caused by Houthi aggression against ships in the strait are likely to redirect maritime traffic from the Suez Canal to alternative passageways. From November to December 2023, the volume of shipping containers that passed through the Canal decreased from 500,000 to 200,000 per day, respectively, representing a reduction of 60%.

Suez Canal Trade Volume Differences (metric tonnes)

The overall trade volume in the Suez Canal has decreased drastically. Between October 7th, 2023, and February 25th, 2024, the channel’s trade volume decreased from 5,265,473 metric tonnes to 2,018,974 metric tonnes. As the weaponization of supply chains becomes part of regional economic power plays, there is a global interest in decreasing the vulnerability of vital choke points via trade route diversification. The lack of transport routes connecting Europe and Asia has hampered these interests, making choke points increasingly susceptible to exploitation.

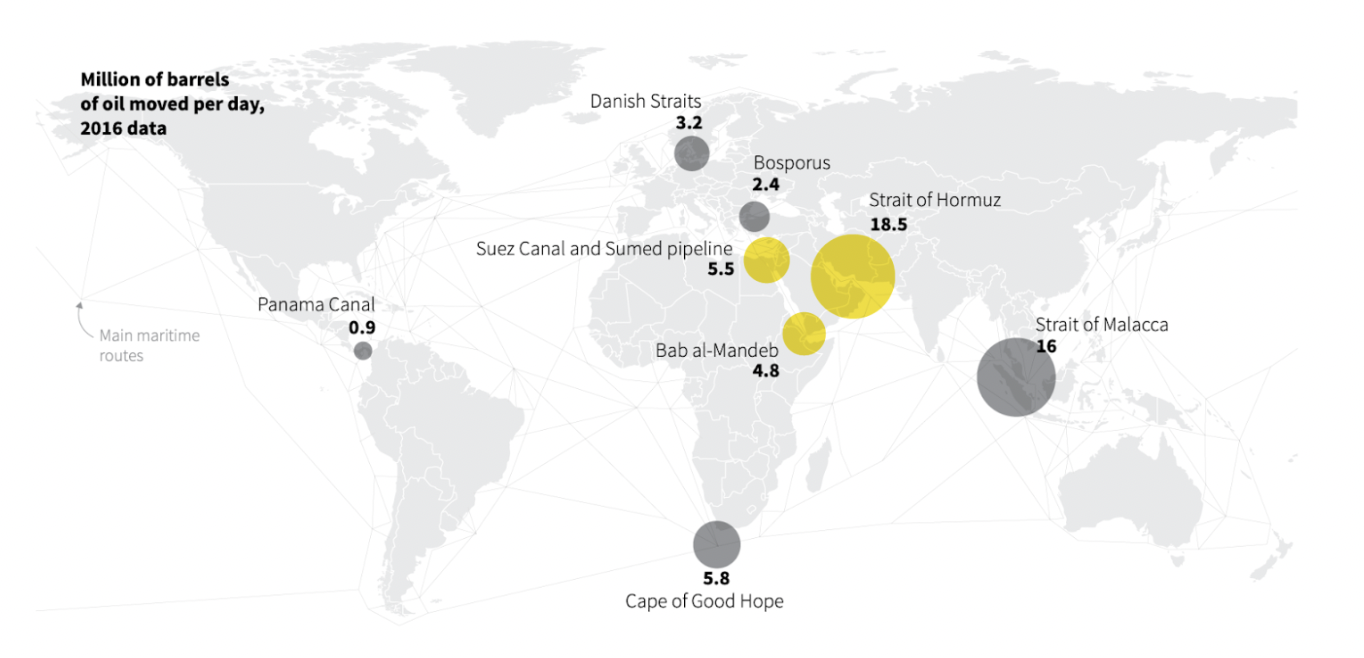

Oil Trade Volumes in Millions of Barrels per Day in Vital Global Chokepoints

Source: Reuters

Quantitative Analysis

Many cargoes have been rerouted through the Cape of Good Hope to avoid the Red Sea region since the beginning of the Houthi conflict. Several European automakers announced reductions in operations due to delays in auto parts produced in Asia, demonstrating the high exposure of sectors dependent on imports from China.

In the first two weeks of 2024, cargo traffic decreased by 30% and tanker oil carriers by 19%. In contrast, transit around the Cape of Good Hope increased by 66% with cargoes and 65% by tankers in the same period. According to the analysis of JP Morgan economists, rerouting will increase transit times by 30% and reduce shipping capacities by 9%.

Depiction of Trade Route Diversion

Source: Al Jazeera

More fuel is used in the rerouted freight, an additional cost that increases the risk of cargo seizure and results in elevated shipping rates. The most affected routes were from Asia towards Europe, with 40% of their bilateral trade traversing the Red Sea. The freight rates of the north of Europe until the Far East, utilising the large ports of China and Singapore, have increased by 235% since mid-December; freights to the Mediterranean countries increased by 243%. Freights of products from China to the US spiked 140% two months into the conflict, from November 2023 to January 25, 2024. The OECD estimates that if the doubling of freight persists for a year, global inflation might rise to 0.4%.

The upward trend in freight rates can be seen in the graphic pictured below, depicting the “Shanghai Containerised Freight Index” (SCFI). The index represents the cost increase in times of crisis, such as at the beginning of the pandemic, when there were shipping and productive constraints, and more recently, with the Houthi rebel attacks. Most shipments through the Red Sea are container goods, accounting for 30% of the total global trade. Companies such as IKEA, Amazon, and Walmart use this route to deliver their Asian-made goods. As large corporations fear logistic and supply chain risk, more crucial trade volumes could be rerouted.

Shanghai Containerized Freight Index

Energy Commodity Impact

Of the commodities that traverse the Red Sea, oil and gas appear to be the most vulnerable. Before the attacks, 12% of the oil trade transited through the Red Sea, with a daily average of 8.2 million barrels. Most of this crude oil comes from the Middle East, destined for European markets, or from Russia, which sends 80% of its total oil exports to Chinese and Indian markets. The amount of oil from the Middle East remained robust in January. Saudi oil is being shipped from Muajjiz (already in the Red Sea) in order to avoid attack-hotspots in the strait of Bab al-Mandeb.

Iraq has been more cautious, contouring the Cape of Good Hope and increasing delays on its cargo. Iraq's oil imports to the region reached 500 thousand barrels per day (kbd) in February, 55% less than the previous year's daily average. Conversely, Iraq's oil imports increased in Asia, signalling a potential reshuffling of transport destinations. Trade with India reached a new high since April 2022 of 1.15 million barrels per day (mbd) in January 2024, a 26% increase from the daily average imports from Iraq's crude.

Brent Crude and WTI Crude Fluctuations

Source: Technopedia

Refined products were also impacted. Usually, 3.5 MBd were shipped via the Suez Canal in 2023, or around 14% of the total global flow. Nearly 15% of the global trade in Naphta passes through the Red Sea, amounting to 450 kbd. One of these cargoes was attacked, the Martin Luanda, laden with Russian naphtha, causing a 130 kbd reduction in January compared with the same month in 2023. Traffic to and from Europe is being diverted in light of the conflict. Jet fuel cargoes sent from India and the Middle East to Europe, amounting to 480 kbd, are avoiding the affected region, circling the Cape of Good Hope.

Due to these extra miles and higher speeds to counteract the delays, bunker fuel sales saw record highs in Singapore and the Middle East. The vessel must use more fuel, and bunker fuel demand increased by 12.1% in a year-over-year comparison in Singapore.

In 2023, eight percent, or 31.7 billion cubic metres (bcm), of the LNG trade traversed the Red Sea. The US and Qatar exports are the most prominent in the Red Sea. After sanctioning Russia's oil because of the Ukrainian War, Europe started to rely more on LNG shipments from the Middle East, mainly from Qatar. The country shipped 15 metric tonnes of LNG via the Red Sea to Europe, representing a share of 19% of the Qatari LNG exports. Vessels travelling to and from Qatar will have to circle the Cape of Good Hope, adding 10–11 days to travel times and negatively impacting cargo transit.

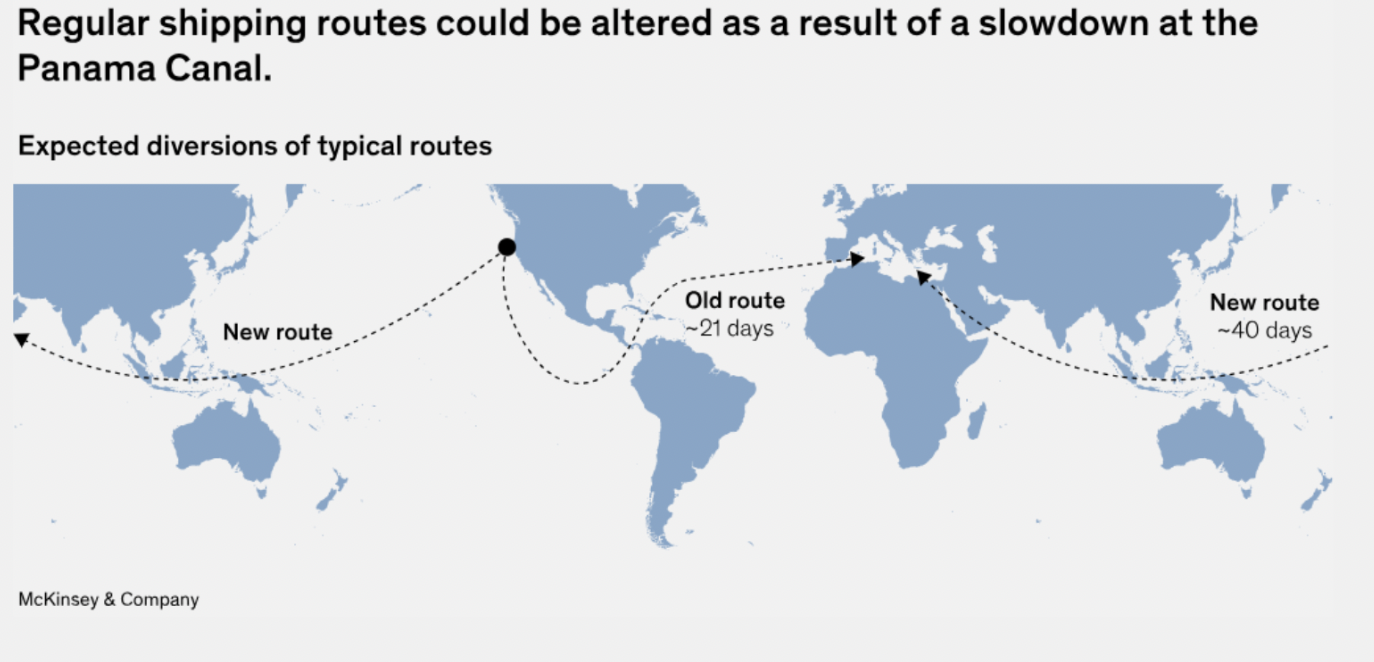

US LNG export capacity has increased in the past few years, sending shipments to Asia via the Red Sea. The Panama Canal receives many LNG cargoes from the US via the Pacific, yet its traffic limitations cause US cargo to be routed through the Atlantic and the Red Sea. The figure “Trade Shipping Routes” below displays the dimensions of the shifts that US LNG cargoes must take in the absence of passage via the Panama Canal.

Trade Shipping Routes

Source: McKinsey & Company

Until January 15, at least 30 LNG tankers were rerouted to pass through the Cape of Good Hope instead. Russia's LNG shipments to Asia are currently avoiding the Red Sea, and Qatar did not send any new shipments in the last fortnight of January after the Western strikes at Houthi targets.

Risk Assessment

A share of 12% of oil tankers, ships designed to carry oil, and 8% of liquified gas pass through this route towards the Mediterranean. Inventories in Europe are still high, but if the crisis persists for several months, energy prices could be aggravated. As evidenced by the sanctions against Russia, cargo reshuffling is possible. Qatar can send its cargoes to Asia, and those from the US can go to European markets, allowing suppliers to effectively avoid the Red Sea.

Around 12% of the seaborn grains traversed the Red Sea, representing monthly grain shipments of 7 megatonnes. The most considerable bulk are wheat and grain exports from the US, Europe, and the Black Sea. Around 4.5 million metric tonnes of grain shipments from December to February avoided the area, with a notable decrease of 40% in wheat exports. The attacks affected Robusta coffee cargoes as well. Cargoes from Vietnam, Indonesia, and India towards Europe were intercepted, impacting shipping prices and incentivizing trade with alternative nations.

Daily arrivals of bulk dry vessels, including iron ore and grain from Asia, were down by 45% on January 28, 2024, and container goods were down by 91%. However, further significant disruptions to agricultural exports are not expected. Most of the exports from the US, a large bulk, were passing through the Suez Canal to avoid the congestion of the Panama Canal due to the droughts that limited the capacity of circulation. These cargoes are now traversing the Cape route.

Around 320 million metric tonnes of bulk sail through Suez, or 7% of the world bulk trade. No significant impacts are predicted for iron ore or coal, which represented 42 and 99 megatonnes of volume, respectively, shipped through the Red Sea in 2023. Most of the dry bulks that traverse the impacted region can be purchased from other suppliers, precluding significant supply disruptions.

As of March 1st, reports show that only grain shipments and Iranian vessels were passing through the Red Sea. There were no oil or LNG shipments with non-Iranian links in the Red Sea. These developments illustrate the significant trade shifts caused by the Red Sea crisis. As of today, a looming threat lies in the Houthis’ promises of large-scale attacks during Ramadan. The lack of intelligence on the Houthi’s military capacity and power makes it difficult to ascertain the extent of future conflicts, generating further uncertainty in commercial trade.

The Strait of Hormuz

The Strait of Hormuz is a channel that connects the Persian Gulf to the Gulf of Oman, providing Iran, Oman, and the UAE with access to maritime traffic and trade. The strait is estimated to carry about one-fifth of the global oil at a daily trade volume of 20.5 million barrels, proving to be of vital strategic importance for Middle Eastern oil supply the world’s largest oil transit chokepoint. The strait is a prominent trade corridor for a myriad of oil-exporting nations, namely the OPEC members Saudi Arabia, Iran, the UAE, Kuwait, and Iraq. These nations export most of their crude oil via the passage, with total volumes reaching 21 mb of crude oil daily, or 21% of total petroleum liquid products. Additionally, Qatar, the largest global exporter of LNG, exports most of its LNG via the Strait.

Geographic Location of Strait of Hormuz

Source: Marketwatch

Although the strait is technically regulated by the 1982 United Nations Convention on the Law of the Sea, Iran has not ratified the agreement. Through its geostrategic placement, Iran can trigger oil price responses through its influence on trade transit, establishing the country’s regional and global influence.

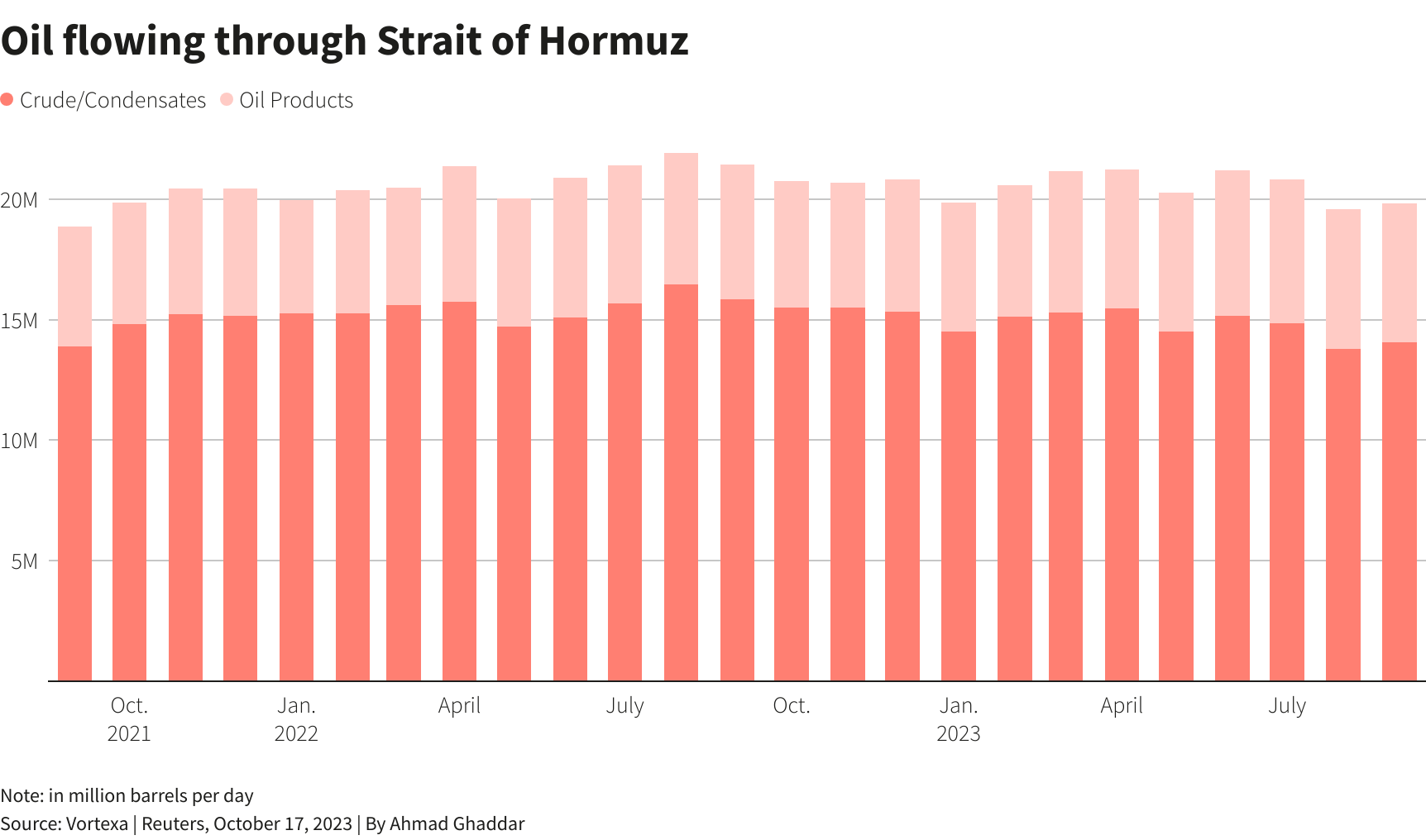

Strait of Hormuz Oil Volumes

Source: Reuters

Experts are particularly worried that the turbulence is likely to spread to the Strait of Hormuz now that Iran backs the Houthis in Yemen and might want to support their cause by doubling down regionally. However, this is something that would cause a lot of backlash in the form of a further tightening of economic sanctions against Tehran, which might deter further provocations.

Despite Iran’s previous threats to block the Strait entirely, these have never gone into effect. Diversifying trade routes to avoid supply shocks and bottlenecks is of interest to regional oil-exporters dependent on the route for maritime trade access. Such diversification attempts have already been undertaken, as seen by the UAE and Saudi Arabia's attempts to bypass the Strait of Hormuz through the construction of alternative oil pipelines. The loss of trade volume from these two producers, holding the world's second and fifth largest oil reserves, respectively, severely hindered the corridor’s prominence.

The attacks on the Red Sea might cause damage to the oil and LNG cargo from countries in the Persian Gulf, increasing costs for oil and gas exporters. However, cargoes could find alternative destinations. The vast Asian markets, which face a shortage of energy products due to a loss of trade through the Red Sea, could be a potential suitor. Finding new LPG (liquefied petroleum gas) contracts could be beneficial for Iran, and its recently enhanced production capacity could supply various markets.

Geopolitics and Prospects for a Route Shift

Although the Strait of Hormuz stands to capture diverted trade flows from the Suez Canal, its global influence is still limited by Iran’s geopolitical ties. As exemplified by the Iran-US conflict, Iran’s conflicts can severely impact traffic through the Strait, significantly impacting the stability of the route and prospects for future growth.

Although security and stability are of paramount importance to trade, efforts to provide these traits could be counterproductive. On March 12th, China and Russia conducted maritime drills and exercises in the Gulf of Oman with naval and aviation vessels. According to Russia's Ministry of Defence, this five-day exercise sought to enhance the security of maritime economic activities using maritime vessels with anti-ship missiles and advanced defence systems. Over 20 vessels were displayed in this joint naval drill, attempting to lure trade through the promise of stability and security.

Whether meant as a display of power or a promise of security, the pronounced presence of Russian and Chinese forces could aggravate geopolitical tensions and increase the potential for conflict in the region, driving global trade prospects down. With precedents of trade conflict, such as the IRGC’s seizure of an American oil cargo in the Persian Gulf on January 22nd, various countries might be sceptical of rerouting commodity trade through the Strait.

Tensions are also aggravated by Iran’s alleged assistance in the Houthi attacks. The US has supposedly communicated indirectly with Iran to urge them to intervene in the region. China and Russia’s interest in improving the Strait’s trade prospects would benefit from a de-escalation of the Houthi conflict, as shown by China’s insistence on Iran’s cooperation in the Houthi conflict. As the conflict stands, the Strait’s prospect as an alternative trade route is dependent not only on Iran’s reputation and presence in global conflicts but also on the route’s patrons and proponents.

Conclusion

The extent to which the Strait of Hormuz could benefit from trade diversion depends not only on its ability to pose itself as a viable trade route but also on the duration of the Houthi conflict. In order to capture trade volumes and increase international trade through the route, Iran would have to ameliorate its geopolitical ties and provide stability to compete with rising prospective trade route alternatives. Although the conflict in the Suez has yet to show promising signs of de-escalation, securing the Suez would likely cause previous trade volumes to resume and restore its hegemony in commodity trade. It remains to be seen whether the conflict will endure long enough to allow other trade routes to be established as alternatives and permanently shift power balances in global trade.

The 2024 BRICS Expansion: Risks & Opportunities

With its 15th summit on August 2023 BRICS gained increased attention. The main focus of the summit was on the potential enlargement of BRICS by admitting new members. During the summit, it was announced that 6 countries - Argentina, Egypt, Ethiopia, Iran, Saudi Arabia, and the United Arab Emirates - had been invited to join the group, with their official entry into the bloc set to take place in January 2024.

The expansion of BRICS has raised questions regarding the implications for international politics and economics. And while most analysts seem to agree that it means something significant, it remains unclear what exactly. This report, therefore, analyses the potential risks and opportunities of the expansion, with a particular focus on the commodities sector. Our analysis addresses questions regarding the interests of BRICS+ countries, the challenges and opportunities for the bloc itself, and the wider commodities sector.

“Protecting America's Strategic Petroleum Reserve from China Act”: Assessing the US Congress’ new idea for depleting Chinese oil markets

On January 12, 2023, the United States House of Representatives passed Bill H.R. 8488, titled the "Protecting America's Strategic Petroleum Reserve from China Act." If enacted, the legislation would prevent the Secretary of Energy from exporting the US strategic petroleum reserve (SPR) “to any entity under the ownership, control, or influence of the Chinese Communist Party”.

The bill received approval with 331 favourable votes and is currently awaiting deliberation by the Senate ever since. The Upper House can either reject or approve the bill and if approved, it would proceed to the President for consideration. This spotlight attempts to clarify the potential impacts on China (if any) in case the Act ever becomes law and restricts its access to imported SPR reserves.

The road ahead on Capitol Hill

The Bill had significant bipartisan support in the Lower House to secure a comfortable majority, with all the 218 present Republicans and about half (113) of present Democrats voting “yes”. Analyst Benjamin Salisbury from Height Capital Markets argues that approval in the Senate might not be so smooth as the Upper House is controlled by Democrats, but it’s still feasible under “tough compromises” - and under greater pressure from voters for a stronger stance against China. The greatest obstacle, however, might arise from the President's Office

President Joe Biden has been depleting the SPRs at an unprecedentedly faster pace to manage oil prices driven up by the war in Ukraine. However, some argue that the move is more about political concerns involved in alleviating inflationary pressures on fuel ahead of an election year. Since the SPRs are only meant to be used in times of great uncertainty and with due restraint - only enough to secure minimal levels of energetic security - critics point out that the President might be compromising the country’s long-term energetic security for short-term political gains. From this point of view, the Executive would hardly sanction a bill that would constrain its influence on oil markets.

But even in a scenario where the Act is approved by both the Legislative and Executive branches, current data suggests that its effects on China’s energy markets are likely to be minimal.

How will China be impacted?

China is the world’s second-largest consumer of crude oil in total volume, and the commodity accounts for roughly 20% of the country’s total energy generation. This figure is roughly comparable to other large emerging economies like India (23%) and Russia (19%). Nevertheless, China represented only one-fifth of the total foreign purchases of SPR released in 2022, while the US itself accounts for only 2% of China’s total crude imports.

Source: S&P Global Commodity Insight

As evident from the chart above, China depends more on oil producers in the Middle East and Eurasia and has concentrated its diplomatic efforts accordingly. It has expanded economic and financial ties with Saudi Arabia, mediated an agreement with Iran, and continues to purchase Russian oil in large quantities. These efforts are likely to provide China with greater resilience against disturbances that may affect energy supplies and limit the US' ability to manipulate oil markets to harm the Chinese economy. Rather than a practical purpose, the act’s eventual approval would likely serve a rhetorical one: Washington is taking a tougher stance against Beijing.

India's Growing Reliance on Russian Oil Imports

Since Russia's full-scale invasion of Ukraine in 2022, India’s reliance on Russian crude oil has increased tenfold. The proportion has risen from as little as 2% of total crude imports in 2021/2022, to 20% in June 2023. Recent estimates suggest that this percentage may reach as high as 30% by the end of the year.

In the wake of the invasion, there has been a largely concerted effort to sanction Russia’s economy and prevent it from further funding their war of aggression. A key component of the sanctions have been directed at Russia’s oil industry, Russia being the world's third largest producer and second largest crude oil exporter.

In December 2022, the EU’s sixth sanctions package came into effect, banning seaborne crude oil and petroleum products from Russia (90% of total oil imports from Russia). This move complimented similar bans enforced in the USA and the UK. Yet an additional component of the combined sanctions effort has been a price cap on Russian crude oil, which set the maximum price at $60 per barrel of crude. Despite the fact that the G7 countries (USA, UK, France, Germany, Italy, Japan, Canada and the EU) have already agreed to ban or phase out Russian crude imports, the cap has given leverage to uninvolved countries, including India, when negotiating prices with Russia.

The rapid increase in Indian imports from Russia suggests that India has been able to harness Russia’s weakened bargaining position. At the same time this new arrangement has put downward pressure on the oil prices charged India’s former suppliers in OPEC, primarily, Iraq and Saudi Arabia

Source: Reuters

The price differential between Russian and OPEC sourced crude, provides a clear basis in explaining India’s shift. Taking the April 2023 price as a point of comparison, India was able to pay as little as $68 per barrel for Russian imported oil, while oil from Iraq (traditionally India’s largest supplier) was priced at $77 per barrel and oil from Saudi Arabia cost as much as $86 per barrel. During the month of April, the overall OPEC basket price ranged from $79 to $86 per barrel. The price gap between OPEC suppliers and Russia makes a clear case for India’s growing imports from Russia, while the significantly lower price of Russian crude demonstrates the impact of the $60 price cap.

Source: Euronews

The challenges posed by India’s growing taste for Russian oil are twofold. In the first instance, while the price of Russian oil is considerably lower than OPEC in this case, the $68 per barrel price tag is still well over the imposed price cap, revealing the limitations of the price cap regime. In the second instance, India has become a rapidly growing market for Russian oil and as such a prop for the Russian war economy. While EU oil imports declined, figure 2 shows the relative increase of Indian oil imports, partially offsetting the impact of oil sanctions. India’s growing reliance on imported Russian oil has already become a point of contention with Western leaders. With the forecasted increase of India’s Russian oil imports, it is likely to remain so.

Image credit: President of Russia via Wikimedia Commons

The 2020s Commodities Boom: How Long Before the Outlook Dives?

The link between commodities boom during recession and inflation is well-established. During a recession, central banks often lower interest rates to stimulate economic activity, which can lead to inflationary pressures. Inflation can also be driven by increased demand for commodities as economies recover. This was evident during the global financial crisis of 2008-2009, where a sharp increase in commodity prices occurred during the recovery phase.

Similarly, the COVID-19 pandemic in 2020 led to a sharp recession, followed by a commodity boom in 2021 due to a combination of factors, including supply chain disruptions and increased demand as economies reopened. The result was a surge in commodity prices, including oil, copper, and agricultural commodities that had continued well into 2023. It is important to highlight these dynamics between economic performance, and commodity rallies, to better outline market performance, and make better long term trading decisions. The link between commodity prices and inflation is made visually available by the St. Louis Federal Reserve.

To project when the outlook in the commodity markets can settle down a time-series analysis must be conducted using historical data to identify trends and patterns in commodity prices, such as the ones above. The analysis must also include macroeconomic variables such as interest rates, inflation, and GDP growth to identify the drivers of commodity prices. However, it is important to note that commodity prices are highly volatile and subject to various unpredictable factors such as natural disasters, political instability, and global events. Yet, based on current trends and projections, it is likely that the commodity boom will eventually settle down as global supply chains stabilise and interest rates cool down. However, the timing and extent of this will depend on a range of factors and will require ongoing monitoring and analysis.

The most likely estimate would be, not before FY2024. Given the reaction of markets to the increase in interest rates, multiple cases of bankruns, the subsequent banking crises, and ongoing Russian invasion of Ukraine, volatility is here to stay for the short-run. However, the CPI (Consumer Price Index) has been showing signs of improvement, with inflation in North America, and the Eurozone, almost at the cusp of weathering down. This follows a decline in energy prices, and can be credited to deflationary fiscal policies aimed at slowing monetary velocity. Given the response of the Federal Reserve, the fallout of the bank failures has been prevented from adding fuel to the fire, and efforts from both banks, and the government, to reassure depositors of confidence in the institutions that govern them, have allowed for the stabilisation of outlook for the short run. To conclude, investors can expect the commodities rallies to continue through 23’, although as economic and geopolitical forces begin to stabilise, the inflated boom can be seen as a short term bubble, waiting to burst as growth returns.

Lithium in Iran: Iranian Gold is Black & White

Iran's Ministry of Industry, Mine, and Trade has declared that a significant discovery of 8.5 million tonnes of lithium has been made in Qahavand, Hamadan. The discovery puts Iran in possession of the largest lithium reserve outside of South America. Furthermore, the Ministry has indicated that there could be even more significant amounts of lithium to be discovered in Hamadan in the future. These developments position Iran to potentially overtake Australia as the top supplier of lithium in the world, although it will be heavily reliant on Iran's diplomatic trajectory.

Background

Lithium is widely referred to as "white gold", similar to petroleum being “black gold”, and is a critical element in the shift towards green energy. It serves as a fundamental component in lithium-ion batteries, the primary energy storage system in electric vehicles (EVs). While lithium-ion batteries have been employed in portable electronic devices for several years, their use in EVs is growing rapidly. By 2030, it is anticipated that 95 per-cent of global lithium demand will be for battery production. However, the price of lithium has been declining for several months, and the recent discovery of Iran's reserve is expected to continue this trend. The extent of the impact on global markets will depend on Iran's ability to export and their production capacity.

Iran's economy is facing significant challenges due to a combination of domestic and international factors. The country has been under severe economic sanctions from the United States since 2018, which has severely impacted its ability to trade with other countries and access the global financial system. The ongoing protests and civil unrest have also taken a toll on Iran's economy. Inflation has been a major problem in Iran, with the annual inflation rate reaching over 40% in 2022. This has led to a decline in the purchasing power of the Iranian currency, the rial, and made it difficult for many Iranians to afford basic necessities.

Analysis

Given Iran's current domestic instabilities, the new find will likely be used as a tool to stabilise the Rial (IRR) which is especially volatile due to international sanctions adversely impacting the country and international political disputes, like the developments linked to the JCPOA. However, as extraction is not planned to begin till 2025, there will not be any real direct short-term economic relief; the government will have to rely on the market’s reaction to future potential.

The discovery will also have diplomatic and foreign policy implications. According to IEA projections, the concentration of lithium demand will be in the United States, the European Union and China. Iran can leverage the necessity of lithium supply to the energy transition and net-zero emission goals as a bargaining chip in future negotiations with Western powers over sanctions relief and its nuclear activities. Iran's growing and diversifying portfolio of essential commodities is a potential threat to those pushing for its exclusion from global trading networks. The new discovery can even act as a catalyst for Iranian membership in BRICS.

China has long-standing economic and political ties with Iran, even amidst Western sanctions. China has been a significant importer of Iranian oil, and in recent years, they have invested heavily in Iranian infrastructure and other sectors. With the discovery of a large lithium reserve in Iran, China is primed to take advantage of its relationship to further pursue its trade interests for rare earth minerals. This could further strengthen the economic ties between the two countries, and also create a new avenue for diplomatic relations. However, the relationship between China and Iran is not without its complications. China's increasing involvement and improved relationship with Iran's regional rivals such as Saudi Arabia has raised concerns in Tehran.

Despite these challenges, the potential economic benefits of the lithium discovery in Iran are significant enough that China is likely to overlook some of these complications and Iran can strengthen its diplomatic ties with political powerhouse. The demand for lithium is expected to increase exponentially in the coming years, particularly in China, which has set ambitious targets for the adoption of electric vehicles. Therefore, the availability of Iranian lithium could be a significant boost to China's domestic EV industry.

Copper Shortages and the Transition to Green Energy

Copper, as a chemical element, is one of the most important because it is especially good at conducting heat and electricity, relative to other metals. It has multiple functions, including its use in industrial machinery and electronic equipment or as a raw material in the development and evolution of clean energies.

Copper, as a chemical element, is one of the most important because it is especially good at conducting heat and electricity, relative to other metals. It has multiple functions, including its use in industrial machinery and electronic equipment or as a raw material in the development and evolution of clean energies. Copper deficit for 2023 has already been announced, and it also symbolizes a period of crisis for plenty of projects and industries. The cause is an evident increase in demand and a severe supply constraint.

Supply-side factors

Most of the world’s suppliers are concentrated in Latin America, where the 10 most important mines are located: Chile (3), Peru (3) and Mexico (1). Unfortunately, a series of recent events have led to a shortage in the supply of copper. In fact, problematical political situations in some of these countries have exacerbated the current deficit. Some of them are:

PERU: It represents 10% of the world's copper supply.

As a consequence of the dismissal of Pedro Castillo for declaring the dissolution of the congress and the state of emergency, some unrest occurred in the last few months, affecting about 30% of copper production.

These are the main mines located in Peru:

- Antamina: It is the largest copper deposit in Peru and represents almost 20% of national production. In 2021, an indefinite suspension of operations was declared due to unrest caused by peasant communities blocking access to the facilities.

- Glencore's Antapaccay: This copper mine has been attacked several times in the first month of 2023 and protesters are demanding the cessation of the mine's operations. As a result, the mine temporarily halted its operations.

- MMG's Las Bambas: The mining company has halted and slowed down copper production due to transportation blockages, as in previous occasions what has been generated is an accumulation of production without being able to dispose of it.

CHILE: The major supplier. It represents 27% of the world copper supply.

Increasing environmental regulation has raised production costs in the mining industry and raised barriers to expansion, as happened with the Dominga mining megaproject due to its environmental impact.

Indeed, companies such as BHP Group, Antofagasta PLC y Freeport-McMoRan Inc. have postponed major investments in this business.

MEXICO: The same stance was adopted. Strict environmental mining regulations have stalled up to 25 major projects by freezing new mining concessions and taking a tougher line on the processing of environmental permits.

Therefore, the main causes of the supply constraints are regulatory concerns about their environmental impact and logistic problems related to the capacity to transport supplies (road blockades and protests) and the chaos generated by the protests, which has forced the suspension or interruption of mining companies’ activities.

In addition, during the first week of February, the operations of First Quantum Minerals, which operated in Panama and is considered one of the largest mines in Latin America, were suspended. The inconveniences this time were caused by disagreements with the Panamanian government in the payment of royalties and taxes.

Demand-side factors

The lack of balance between supply and demand is also due to the simultaneous increase in copper consumption in China, driven by a growth in its economic expansion, and its reopening of the market after the pandemic period. China is the world's largest copper consumer and has increased its demand due to the large investments and infrastructure projects that are on the way.

Along the same lines is the global project to move towards a green energy transition. In accordance with the 2030 Agenda for Sustainable Development (SGD), adopted by the member states of the United Nations and the goals set for 2050, a series of projects have been launched to achieve an efficient energy transition. In light of this planned transiation, copper has become an essential resource as it is essential for the replacement of fossil fuel-based power systems with renewable energy sources.

Therefore, the energy transition has led to a huge demand for copper. Indeed, annual demand will double to 50 million tons by 2035, raising the concern that shortages could result in a reversal of the course of the energy transition. This been seen already in industries such as as construction, manufacturing, architecture. Additionally, the automotive sector’s ability to produce electric vehicles on a large scale will be especially hindered by such shortages.

Summary

The halt in production in the world's main copper-producing regions has exacerbated the impact of increasing demand for copper. Cash-settlement prices for copper listed on the London Metal Exchange (LME) show a rapid increase in copper prices from $5,965 to $8,387 in the period between end of year 2018 to end of year 2022.So far this quarter the LME’s copper cash-settlements peaked at $9.436 on January 18. Experts predict that the price will remain above US$8,500 per tonne for the next few years, with the risk of even exceeding US$10,000.

Unfortunately, a similar situation may occur with other relevant minerals such as lithium and cobalt. In fact, copper experience will be a clear reference for other raw materials in order to find an effective solution.

In the end, it is all about balancing the dilemma between the environmental, social and governance (ESG) practices that are the main challenges of mining and increasing copper production to supply key sectors of the green transition and the economy.

All in all, the supply of copper will be substantially impaired by the following factors:

Copper is a necessary element in many manufacturing and construction industries, added to the growing demand in renewable energy projects that use this element as part of the transition.

The demand for copper from high consuming countries such as China will cause the supply and demand balance to become more unbalanced if a controlled supply solution is not found.

The lack of consensus between the private sector, the public sector and communities around mining will maintain the constant blockades and protests in the main copper-supplying cities in Latin America.

Environmental regulation is increasingly relevant for the development of the mining activity but has become a barrier to its operation.

The cessation of activities of the main mining companies abruptly generates a deficit in the copper supply, which has a direct impact on the price of copper, given the scarcity situation, expanding the damage caused by the initial problem.

Climate Policies for the Shipping Industry: What They Mean for Global Supply Chains

Just as businesses throughout the world grapple with the effects of the coronavirus pandemic and the Ukraine crisis on global supply chains, another issue looms: new emissions standards that promise to affect how shippers run numerous transoceanic and regional channels.

Decarbonization is a costly endeavour, but the European Union (EU) seems willing to make the sacrifice. The European Commission offered a variety of options in July 2021 to help the EU accomplish its objective of decreasing greenhouse gas (GHG) emissions by 55% by 2030 compared to 1990 levels.

One such policy would eliminate free allowances for cement, iron, steel, fertiliser, and aluminum producers and instead assess import duties on these items based on their carbon footprint. This so-called carbon border adjustment mechanism (CBAM) attempts to even out the playing field by requiring other nations around the world exporting to the EU to account for the carbon they generate whilst exporting steel. CBAM is typically imposed and regulated by the recipient country, which imposes a carbon tax on some imported commodities at a rate equivalent to that of comparable local products.

To add to the difficulties, the EU intends to include ships in its Emissions Trading System (ETS) in 2023. For journeys between EU and non-EU ports, shipping corporations will be required to purchase licenses for 50% of emissions. Danish shipping giant Maersk has already declared tariffs for its trade lanes from Asia to North Europe and North Europe to the United States, and others will be required to jump on board. While an impending economic downturn is already bringing down shipping rates, they are unlikely to revert to pre-pandemic values in the long run because the additional expenditures must be paid for.

For managers planning their supply chains, there are several important things to pay attention to:

The costs of carbon reduction in maritime transport will alter the economics of where commodities are sourced. Although spot market rates have lately decreased, it is certainly impossible to expect cost to return to pre-pandemic levels. While carriers want to add significant new capacities in the coming years, forecasting shipping prices is difficult since the retirement of ageing capacity that will have difficulty following the ETS standards would likely balance out the increases. Much will depend on whether import demand in the United States falls and carriers choose to idle ships. Other industries, such as bulk carriers and vessels for transporting motor vehicles, may face substantial hurdles due to a lack of a robust order book for newer, more efficient vessels to supplant older ones that must be retired. High-volume trade corridors where container lines could employ newer, larger, and more efficient infrastructure will perform better, but overall, even if manufacturing costs are lower, it could make less sense to produce hundreds of products far away from where they will be consumed.

Lower-volume trade corridors will probably see fewer and more expensive services. This was anticipated in 2021, at the peak of the supply chain crises, when Japan lost certain direct eastbound connections to North America as container lines attempted to juggle capacity constraints and delays by eliminating port visits from their scheduled rotations (a more efficient technique of running the ships). The ETS rules will favour efficiency by allowing for larger ships, fewer port visits, and less frequent service while maximising capacity utilisation per ship.

Companies that export to Europe or have European suppliers should budget for the greater expenses that CBAM, ETS, and other countries' initiatives will impose. Managers must expect other nations outside the EU to adopt similar steps. Managers in the United States, for example, must pay heed to Canada, which has mandated a significant increase in carbon pricing for 2030. Comparable border adjustment methods may come under pressure in heavy-GHG-emitting industries like the steel industry.

As explained above, carbon transition policies and laws are expected to have a significant impact on the structure of supply chains. Cost increases and the practicalities of shipping logistics are both on the rise. Therefore, now is the time to start planning for this new age.

Image credit: Eric Kilby via Flickr

Adding palm-oil to the fire: Malaysia’s proposed ban of palm oil exports to the EU

On 9 January 2023, both Malaysia and Indonesia’s heads of government agreed to work together to “fight discrimination against palm oil”, in a reference to new European Union anti-deforestation legislation. Tangibly, the Malaysian plantation and commodities minister is threatening a wholesale ban on palm oil exports to the EU. Given that Malaysia and Indonesia combine for more than 80 per cent of the world’s palm oil supply and the EU is their third-largest market, the potential ramifications for any such moves would be significant.

How has an issue over palm oil trade reached such a point? For years, Malaysia and Indonesia have railed against EU import barriers on their palm oil, which they characterise as protectionist in favour of the EU’s domestic vegetable oil sector. The EU’s new law, which is expected to be implemented late 2024, obligates “companies to ensure that a series of products sold in the EU do not come from deforested land anywhere in the world” and is aimed at reducing the EU’s impact on biodiversity loss and global climate change. Whilst no country or commodity is explicitly banned, the new regulation covers palm oil and a number of its derivatives. Currently, both Malaysia and Indonesia have separate lawsuits at the World Trade Organization (WTO) pending over the EU’s palm oil trade restrictions.

Implications

To date, only Malaysia has explicitly threatened to ban palm oil exports to the EU. Were this issue to escalate and Malaysia to impose the suggested ban, it would have several consequences. First and foremost, Malaysia’s palm oil industry and wider economy would be hit; the industry makes up 5 per cent of Malaysian GDP, of which a non-negligeable 9.4 per cent of its exports are bought by the EU. Additionally, an abrupt ban is likely to harm producers who have contracts to sell in the EU. Alternative export destinations could be found, especially in food-importing markets such as the Middle East and North Africa, but these producers would struggle to pivot in the short-term and likely see financial losses. Even greater disruptions would be experienced by the few Malaysian palm oil companies that have established refineries in Europe, necessitating a reorientation in their supply chains. Yet the outlook is not entirely negative; palm oil’s lower cost as compared to its substitutes such as soybean oil or sunflower oil will sustain global demand. Overall the Malaysian export ban to the EU would cause a limited scope of economic damage in the short-term, and would see gradually less impact as time progresses and firms adjust.

The potential implications for the EU are equally significant. Firstly, if Malaysia were to enact an export ban soon, this would likely be in unison with Indonesia as the larger producer. A unilateral Malaysian palm oil export ban to the EU, with new regulations permitting, would simply lead EU imports to shift to Indonesia along with profits - hence Malaysia is seeking bilateral action. A joint ban on exporting to the EU would cut the EU off from around 70 per cent of its palm oil, meaning significant interruptions in processed food or biofuel production. New import regulations, however, will help the EU’s domestic vegetable oil sector, which is something that Malaysia asserts. Especially in biofuel production, oils such as soy, canola, and rapeseed would fill the palm oil gap and increase their respective market shares. This issue is further complicated by the EU and Indonesia seeking an elusive free-trade agreement, with negotiations routinely stalled by the EU’s palm oil regulations. This could be in the EU’s favour as free-trade negotiations would break Indonesian-Malaysian solidarity on the issue.

Ironically, the EU’s new regulation could also result in greater amounts of deforestation, instead of less. As the EU reduces its palm oil imports through stricter environmental regulations, Malaysian and Indonesian exports would shift even more to the two larger importers in India and China, with less stringent environmental regulations. The EU’s citizens may not be as directly responsible for deforestation, but worldwide deforestation may in fact increase as a result of this policy.

Market forecast

The immediate reaction from markets was nonplussed. Traders don’t see the threat of an export ban from Malaysia holding. This is reflected in palm oil futures contracts (FCPO: Bursa Malaysia Derivatives Exchange, the benchmark for palm oil), where prices remained stable since the EU’s law was proposed and Malaysia’s threat issued. This means the ban is currently not taken seriously, with Malaysian threats interpreted as a knee-jerk reaction. In any case, firms are anticipating decreased demand from the EU and have been exploring new markets to offset potential European losses. If this Malaysian export ban to the EU were to happen, this would nonetheless pale in comparison to the supply shocks experienced in 2022. A brief ban on all Indonesian palm oil exports globally in April 2022, amidst fears of food shortages and high domestic prices, resulted in record-high global prices. This is a level we are unlikely to see again, as stability returns.

On the supply-side the Malaysian Palm Oil Council expects production to recover in 2023 with estimates of a 3-5 per cent increase, after three years of decline amidst labour shortages linked to COVID-19. This is likely to have a greater impact on global markets instead of a ban or the threat of one, and both Malaysia and Indonesia’s output will continue to climb in the years to come.

Forecasting the demand side is more uncertain. Short-term projections suggest lower demand due to China’s surge of COVID-19 infections post-Lunar New Year, but this is more symptomatic of the wider Chinese economic reopening which will, on balance, stimulate demand. In the medium-term, the threat of recession facing the global economy will hurt palm oil demand, with a mild recession expected in the first half of 2023 followed by a gentle recovery. A longer-term positive outlook is observed in relation to biodiesel’s potential. Amidst high crude oil prices, the further development of biodiesel utilising palm oil would incite new demand.

Looking ahead, projections are uncertain given factors such as the Malaysian migrant worker shortage, the Chinese economy reopening, and potential global recession. This is in addition to Malaysia and Indonesia’s unpredictable regulatory environment, where any policy is subject to rapid change. Palm oil exports to the EU are likely to remain a point of contention between the two south-east Asian countries and their European counterparts. Because palm oil forms a significant part of Malaysia and Indonesia’s economies, their respective governments will continue to intervene.

As the two largest producers in this market potential cooperation between Malaysia and Indonesia over an EU export ban must be monitored- acting together would result in greater consequences for EU imports and worldwide prices. While the Malaysian threat to ban exports to the EU may be an empty one, decreased EU palm oil imports will be observed as it shifts towards more sustainable consumption. Combating climate change is the EU’s underlying aim, but this will necessitate a change in trade patterns.