Australian Mining in Crisis: Nickel’s Price Plunge

On February 16th, Australia added nickel to its Critical Minerals List to protect its mining industry from strong competition from low-cost Indonesian nickel. Indonesia’s nickel industry is expected to continue growing, backed by pursuant investments from China. Australia’s inclusion of nickel makes the mineral eligible for a 3.9 billion-dollar fund to support the minerals industries linked to the energy transition through grants and loans with low-interest rates. This inclusion is a response to the persistent downward trend of nickel prices that began at the end of 2022, caused by an increase in the supply of cheaper nickel produced in Indonesia. Nickel is used to manufacture batteries for electrical vehicles (EVs) and stainless steel. However, the low-profit margin of nickel exploitation, in combination with increased competition from Indonesia, is jeopardising the Australian mining industry and pushing investors away from Australian mines.

Chinese Investment Into Indonesian Nickel And Its Impacts On Australia

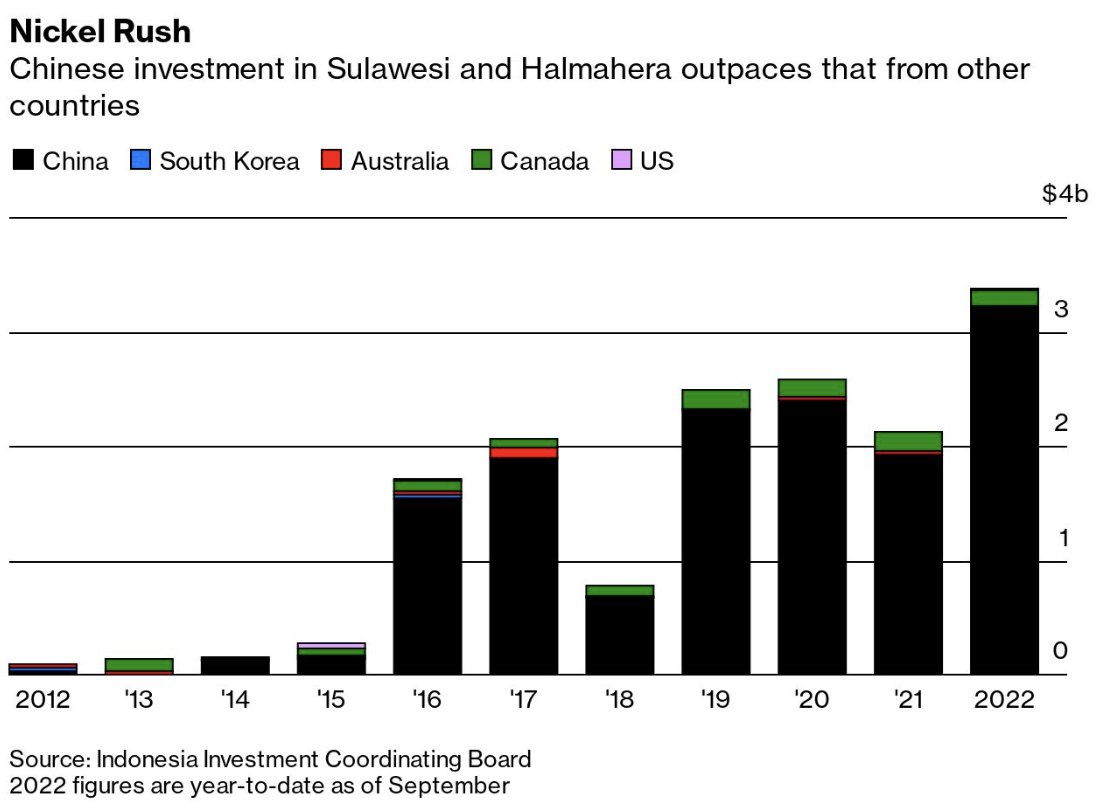

One of the biggest reasons for the global decline in nickel prices, which decreased by 45% in the past year, is Chinese investment in Indonesia. In 2020, Indonesia–which holds 42% of the global nickel reserves–reinstated a ban on unprocessed nickel exports to encourage onshore investment in its processing industry. Large multinational companies, such as Ford and Hyundai, invested in ore processing and manufacturing in the archipelago to access its nickel reserves. Indonesian lateritic nickel ore is attractive as it is closer to the surface than the sulphide ore found in Australia or Canada, making the required infrastructure to exploit it significantly cheaper. The sector received massive Chinese investments in various forms, such as refineries, smelters, and metallurgic schools, to develop the industry that had not previously evolved due to the lack of business know-how and financial investments. In 2022, Chinese investments accounted for 94.1% of the total foreign direct investments in the Indonesian reserves, as seen in the “Nickel Rush” chart below. The investments increased quickly after the ban on unprocessed Indonesian nickel in 2014, which was later eased. These investments boosted the production efficiency of Indonesian refined and semi-refined nickel, representing 55% of the world's total nickel supply in 2023 and potentially increasing its market share to 75% by 2030.

The chart can be found here.

The investment inflows towards Indonesian nickel also helped its laterite nickel ore to become more competitive compared to foreign ones. Primary nickel production is divided into two grades: (1) low-grade or Class II, which is used to manufacture stainless steel and found mainly in Indonesia, and (2) high-grade or Class I, which is used in batteries and can be found in Canada and Australia. While Indonesia has an abundant reserve of low-grade nickel, investments in the industry enabled its producers to apply sophisticated methods to upgrade its nickel to a higher grade. With the improved quality, this type of nickel can be used for batteries, after applying high temperature and pressure methods called high-pressure acid leaching (HPAL), allowing the Indonesian nickel to compete with other countries.

Global Challenges Impacting Nickel Demand

From the demand side, China, Europe, and the United States–Australia’s largest nickel importers—are simultaneously experiencing reduced demand for various reasons. The stainless steel market, which accounts for 75% of nickel use, was sluggish in 2023 due to a slow economic recovery in Europe and the US, which are still recovering from pre-COVID levels. Demand is set to increase by 8% in 2024, but the oversupply mutes its effects. As Sino-American tensions grow, China, the biggest EV market, faces deep and complex economic challenges, including a lack of trust from investors and buyers. Europe, the second biggest EV consumer, has seen the end of tax breaks and other government incentives to buy EVs. Moreover, the US’ high-interest rates prevent consumers from taking out loans, including for EV purchases. The combination of these factors is plummeting the aggregate demand for EVs, thus further pushing down nickel prices, an important mineral for EV batteries.

Consequently, Australian nickel mines are becoming uncompetitive at the current price range, with many even shutting down as nickel prices are expected to continue decreasing throughout 2024. The unit cost per ton of Australian nickel is 28% higher than in Indonesia. Also, while nickel prices decreased globally, its Australian production cost has increased by 49% since 2019, driven by rising wages. The London Metal Exchange (LME) listed nickel closed at US$16.356 per metric ton on February 16, a downward trend since its peak of around US$33,000 per metric ton in December 2022, as seen in the chart below. Companies such as IGO, First Quantum, and Wyloo Metals, some of the most prominent actors in Australian nickel mining, have pulled back investments or suspended part of their businesses.

Chart made by the author with data from Investing.com

These recent developments threaten the jobs of many Australian workers. BHP, the largest Australian mining company, recently announced it may take an impairment charge of around US$3.5 billion. The company plans to shut down its Nickel West division, which employs nearly 3,000 people. In total, the Australian nickel industry supported 10,000 jobs in 2023.

The situation is not exclusive to Australia. Eramet, a French mining company, lost 85% in revenue in 2023 in its New Caledonia nickel plant without any prospect of having government aid to increase its competitiveness. Macquarie, an asset management firm, estimates that 7% of the total nickel production has been removed due to closures. Even so, Australia will likely be the most affected. The country has 18% of global nickel reserves, but it is no longer competitive and is left contemplating the potential of its uncompetitive reserves.

The Debate Over 'Dirty' vs 'Clean' Nickel

There may be a solution to Australia’s nickel problem beyond access to the Australian Critical Mineral Facility Fund. Australian nickel producers are subjected to more strict sustainable standards than Indonesia, increasing costs. The refining of Australian nickel produces six times fewer emissions than other countries, including Indonesia. For these reasons, Madeleine King, the Australian Resources minister, urged the LME to split the listing of nickel into two categories: “dirty” coal-produced nickel and “clean” green nickel. Mining businessmen also demand this separation to motivate buyers to pay a premium for Australian and other nickel supplies with a smaller carbon footprint to level the competition against Indonesian nickel with this premium. This type of split in mineral contracts already exists, such as for aluminium and copper.

LME officials also declare that classifying minerals according to ESG criteria is a tough challenge given the lack of a universal ESG standard. Currently, carbon emissions per ton of the nickel listed in the LME vary greatly, from 6 to 100 tons of carbon dioxide per ton of nickel produced, and the lack of a standard makes it difficult to estimate the absolute emissions that would classify a nickel as “clean”. Currently, the LME classifies low-carbon nickel as producing less than 20 tons of carbon dioxide per ton, and it is working on a more precise definition with nickel specialists.

Reshaping the Australian nickel industry

It is unlikely that the LME will list green nickel separately from “dirty” nickel soon, given the liquidity threats this incurs. The broker wants to solidify buyers' confidence after the 2022 nickel episode before making changes that can jeopardise liquidity. LME officials stated in mid-March of this year that they have no plans to do so as the market size of a green nickel is not large enough to split it. On the other hand, Metalhub, a digital broker, recently started to split its nickel listing with the support of the LME. MetalHub allows the producers to have an ESG certificate tailored to their emissions per ton, which is more flexible than the LME ESG standards. The demand for the “clean” nickel in the digital broker would determine an index price used to derive the premium for this product type and delimit the liquidity of this trade contract. The digital broker plans to release the contract data when the volume traded increases.

It will be challenging to see nickel prices at levels that would make Australia's nickel mining industry competitive again. Indonesia is not hiding the fact that it wants to influence market prices with its nickel supply. According to Septian Hario Seto, an Indonesian deputy overseeing mining, the current price allows Indonesian nickel producers to sustain their activities. Also, low nickel prices will lower the costs of its emerging battery industry, completing the strategy to build an Indonesian upstream industry of batteries.

The access to Australia’s Critical Minerals Facility fund, in combination with the Inflation Reduction Act (IRA) from the US, brings the expectation of an increase in investment towards the nickel industry. The Australian fund will be crucial to leverage projects to reduce costs by increasing productivity and infrastructure efficiency related to high costs such as energy, water, high-skilled labour, and transport. Also, the US’ IRA is set to increase the demand for Australian nickel, as it obliges US industries to purchase 40% of its critical minerals needs from either domestic producers or countries with which the US has a free trade agreement–wherein Australia is one of them. The two, combined with ever-evolving environmental regulations leading to a greater demand for EVs, can bring the required financial boost for Australia’s upstream nickel production. However, it will be more difficult for its nickel downstream industry given internal inflation and external competition not only from Indonesia but from all the countries building plans to rebuild their national processing industries.

When it comes to nickel buyers, assuming standard market incentives, they will pay more if they see an advantage in buying a cleaner metal, such as government subsidies or a bigger profit margin on selling a greener EV. Summing up, Australia chose to include nickel in its Critical Minerals List, assuming a big part of the responsibility to protect the industry. The government is one of the stakeholders with the financial ability and the incentive to avoid adverse socioeconomic developments. Minister King is also working with counterparts to advocate for robust standards in production to be reflected in a price premium. These counterparts–namely the US, the EU, and Canada–have the same interest in building an alternative supply chain to the Chinese one. The combination of factors such as the Critical Mineral Facility Fund, the IRA, and a possible stable price premium will give much-needed relief to persisting uncompetitive problems faced by Australian nickel producers. This seems to be the beginning of a pathway towards enhanced competitiveness for Australian nickel miners and, possibly, more sustainable nickel standards.

Even so, more funds might be insufficient to make the Australian nickel miners more competitive. Indonesia has a competitive advantage with a low production price that incurs high costs to its citizens. Coal mines are being constructed to fuel energy-intensive activities to upgrade the Indonesian nickel, making the country reach record levels of coal consumption and carbon emissions. Rivers are contaminated with heavy metals from the mines and refineries, exposing inadequate waste disposals. Addressing these environmental and social costs will level up Indonesian nickel prices, indirectly benefiting Australia and promising relief for the communities burdened by these impacts.

M23: How a local armed rebel group in the DRC is altering the global mining sector

In recent weeks, North Kivu, a province in the eastern part of the Democratic Republic of Congo (DRC), has seen over 135,000 displacements in what has become the latest upsurge in a resurging conflict between the Congolese army and armed rebel groups. The indiscriminate bombing in the region puts an extra strain on the already-lacking humanitarian infrastructure in North Kivu, which thus far harbours approximately 2.5 million forcibly displaced people.

The March 23 Movement, or M23, is an armed rebel group that is threatening to take the strategic town of Sake, which is located a mere 27 kilometres west of North Kivu’s capital, Goma, a city of around two million people. In 2023, M23 became the most active non-state large actor in the DRC. Further advances will exacerbate regional humanitarian needs and could push millions more into displacement.

The role of minerals

Eastern Congo is a region that has been plagued with armed violence and mass killings for decades. Over 120 armed groups scramble for access to land, resources, and power. Central to the region, as well as the M23 conflict, is the DRC’s mining industry, which holds untapped deposits of raw minerals–estimated to be worth upwards of US$24 trillion. The recent increase in armed conflict in the region is likely to worsen the production output of the DRC’s mining sector, which accounts for 30 per cent of the country’s GDP and about 98 per cent of the country’s total exports.

The area wherein the wider Kivu Conflicts have unfolded in the last decade overlaps almost entirely with some of the DRC’s most valuable mineral deposits, as armed groups actively exploit these resources for further gain.

The artisanal and small-scale mining (ASM) sector produces about 90 per cent of the DRC’s mineral output. As the ASM sector typically lacks the size and security needed to efficiently deter influence from regional rebel groups, the mining sector as a whole falls victim to instability as a result of the M23 upsurge. Armed conflict and intervention by armed groups impacts 52 per cent of the mining sites in Eastern Congo, which manifests in the form of illegal taxation and extortion. As such, further acquisitions by M23 in Eastern Congo may put the DRC’s mineral sector under further strain.

The United Nations troop withdrawal

The escalation of the M23 conflict coincides with the United Nations’ plan to pull the entirety of their 13,500 peacekeeping troops out of the region by the end of the year upon the request of the recently re-elected government. With UN troops withdrawn, a military power vacuum is likely to form, thereby worsening insecurity and further damaging the DRC’s mining sector. However, regional armed groups are not the only actors that can clog this gap.

Regional international involvement

A further problem for the DRC’s mining sector is that the country’s political centre, Kinshasa, is located more than 1,600 km away from North Kivu, while Uganda and Rwanda share a border with the province.

Figure: Air travel distance between Goma and Kinshasa, Kigali and Kampala (image has been altered from the original)

The distance limits the government’s on-the-ground understanding of regional developments, including the extent of the involvement of armed groups in the ASM sector, thereby restricting the Congolese military’s effectiveness in countering regional rebellions.

In 2022, UN experts found ‘solid evidence’ that indicates that Rwanda is backing M23 fighters by aiding them with funding, training, and equipment provisions. Despite denials from both Kigali and M23 in explicit collaboration, Rwanda admitted to having military installments in eastern Congo. Rwanda claims that the installments act as a means to defend themselves from the Democratic Forces for the Liberation of Rwanda (FDLR)–an armed rebel group that Kigali asserts includes members who were complicit in the Rwandan genocide. The FDLR serves as a major threat to Kigali’s security, as its main stated aim is to overthrow the Rwandan government.

As such, M23, on the other hand, provides Rwanda with the opportunity to assert influence in the region and limit FDLR’s regional influence. Tensions between Rwanda and the DRC have, therefore, heightened, especially with the added fact that the Congolese army has provided FDLR with direct support to help the armed group fight against M23 rebels. As such, the DRC has been accused of utilising the FDLR as a proxy to counter Rwandan financial interests in the Congolese mining sector.

Another major point of contention between the states involves the smuggling of minerals. The DRC’s finance minister, Nicolas Kazadi, claimed Rwanda exported approximately $1bn in gold, as well as tin, tungsten, and tantalum (3T). The US Treasury has previously estimated that over 90 per cent of DRC’s gold is smuggled to neighbouring countries such as Uganda and Rwanda to undergo refinery processes before being exported, mainly to the UAE. Rwanda has repeatedly denied the allegations.

Furthermore, the tumultuous environment caused by the conflict might foster even weaker checks-and-balance systems, which will exacerbate corruption and mineral trafficking, which is already a serious issue regionally.

In previous surges of Congolese armed rebel violence, global demand for Congolese minerals plummeted, as companies sought to avoid problematic ‘conflict minerals’. In 2011, sales of tin ore from North Kivu decreased by 90 per cent in one month. Similar trends can be anticipated if the M23 rebellion gains strength, which may create a global market vacuum for other state’s exports to fill.

China

In recent years, China gained an economic stronghold of the DRC’s mining sector, as a vast majority of previously US-owned mines were sold off to China during the Obama and Trump administrations. It is estimated that Chinese companies control between 40 to 50 per cent of the DRC’s cobalt production alone. In an interest to protect its economic stakes, China sold nine CH-4 attack drones to the DRC back in February 2023, which the Congolese army utilised to curb the M23 expansion. Furthermore, Uganda has purchased Chinese arms, which it uses to carry out military operations inside of the DRC to counter the attacks of the Allied Democratic Forces (ADF), a Ugandan rebel group, which is based in the DRC. In return for military support, the DRC has granted China compensation via further access to its mining sector, which is helping bolster China’s mass production of electronics and technology within the green sector.

The US

Meanwhile, the US has put forth restrictions on imports of ‘conflict minerals’, which are minerals mined in conflict-ridden regions in DRC for the profit of armed groups. Although the US attempts to maintain certain levels of mineral trade with the DRC, the US’s influence in the country will likely continue to phase out and be overtaken by Beijing. The growing influence of M23 paves the path for further future collaboration between China and the DRC, both militarily and economically within the mining sector.

The UAE

The UAE, which is a major destination for smuggled minerals through Rwanda and Uganda, has since sought to end the illicit movement of Congolese precious metals via a joint venture that aims to export ‘fair gold’ directly from Congo to the UAE. In December of 2022, the UAE and DRC signed a 25-year contract over export rights for artisanally mined ores. The policy benefits both the DRC and the UAE as the UAE positions itself as a reliable partner in Kinshasa’s eyes, which paves the path for further business collaboration. In 2023, the UAE sealed a $1.9bn deal with a state-owned Congolese mining company in Congo that seeks to develop at least four mines in eastern DRC. The move can be interpreted as part of the UAE’s greater goal to increase its influence within the African mining sector.

Global Shifts

China and the UAE’s increasing involvement in the DRC can be seen as part of a greater diversification trend within the mining sector. Both states are particularly interested in securing a stronghold on the African mining sector, which can provide a steady and relatively cheap supply of precious metals needed to bolster the UAE’s and China’s renewables and vehicle production sectors. The scramble for control over minerals in Congo is part of the larger trend squeezing Western investment out of the African mining sector.

Furthermore, the UAE’s increasing influence in the DRC is representative of a larger trend of the Middle East gaining more traction as a rival to Chinese investment in Africa. Certain African leaders have even expressed interest in the Gulf states becoming the “New China” regionally, as Africa seeks alternatives to Western aid and Chinese loans.

Although Middle Eastern investment is far from overtaking China’s dominance of the global mining sector, an interest from Africa in diversifying their mining investor pools can go a long way in changing the investor share continentally. Furthermore, if the Middle East is to bolster its stance as a mining investor, Africa serves as a strategic starting point as China’s influence in the African mining sector is at times overstated. In 2018, China is estimated to have controlled less than 7 per cent of the value of total African mine production. Regardless, China’s strong grip on the global mining sector might be increasingly challenged through investor diversification in the African mining sector. The DRC is an informant of such a potential trend.

The further spread of the M23 rebellion, though likely to damage the Congolese mining business, might also foster stronger relations with countries such as the UAE which seek to minimise ‘conflict mineral’ imports. As such, the spread of the M23 rebellion–which acts as a breeding ground for smuggling, might catalyse new and stronger trade relations with the Middle East. This could be indicative of a trend of “de-Chinafication” in the region, or at least greater inter-regional competition for investment into the African mining sector.

Sinking shores and rising concerns: the environmental fallout of sea sand mining

Urbanisation is one of the contemporary era’s defining trends, with urban populations previously comprising 29% of the world’s inhabitants in 1950, as compared to 56% today and a predicted 70% by 2045. The astounding influx of populations into urban areas is accompanied by large-scale construction projects for infrastructure, industrial, commercial, and residential developments, which raises environmental concerns at various levels. One concern pertains to the large amounts of sand needed as a key ingredient of concrete and asphalt. In 2021, the United States, Australia, Malaysia, the Netherlands, and Germany were the largest net exporters of sand, while China, Canada, Japan, Singapore, and Italy were the largest net importers, driven by high rates of urban construction and land reclamation.

The high demand for abundant and easily accessible sand has prompted the need for sea sand mining, which involves the extraction of sand from ocean floors. However, this increasingly prevalent practice brings significant correlated environmental issues and ecological disruption. Extraction activities disturb the delicate balance of marine habitats, destroying coral reefs, seagrass beds, and other essential marine organisms. These ecosystems play a crucial role in maintaining biodiversity, providing food sources, and protecting coastal areas from erosion and storm surges. The destruction of these habitats can lead to the loss of species, damage to coastal areas, and increased vulnerability to natural disasters. Alongside habitat destruction, sea sand mining also contributes to climate change, in that the extraction process releases large amounts of carbon dioxide into the atmosphere, mainly through the use of heavy machinery and transportation. Additionally, the removal of sand from coastal areas can disrupt the natural sediment flow, altering coastal dynamics and increasing the risk of erosion and flooding. These changes have huge implications for the stability of coastal ecosystems, the livelihoods of coastal communities, and the overall resilience of coastal regions in the face of climate change impacts.

Recognising the detrimental effects of sea sand mining, Indonesia banned exports of sea sand in 2003 and consolidated the ban in 2007 with regulations against illegal shipments. Prior to the ban, Indonesia was Singapore’s main supplier of sea sand for land reclamation, shipping more than 53 million tonnes on average per year between 1997 to 2002. Sand mining, coupled with persistently rising sea levels, had caused several islands in the Thousand Islands regency – located north of Jakarta – and the Riau Islands to sink underwater.

However, in late May, Indonesia lifted the ban in desperate hopes of attracting economic benefits to the country. This move comes a few years after Malaysia banned sea sand exports in late 2019, which complicated Singapore’s ambitious land reclamation plans. After Indonesia’s 2003 ban, Singapore turned to Malaysia to import sand, which by 2021 comprised nearly 63% of Singapore’s sand imports. For this reason, Malaysia’s recent ban gave Indonesia a window of opportunity to reattract revenue from sand exports to the region, especially to supplement Singapore’s expansion plans. Mining permit holders are now permitted to collect and export sea sand, provided that domestic demands have been met. Environmentalists, including Indonesia’s former Maritime Affairs and Fisheries Minister, Susi Pudjiastuti, have condemned the reversal of the sea sand mining ban. Greenpeace Southeast Asia labelled the move as ‘greenwashing’, inasmuch as the Indonesian government claims their decision will aid in improved sustainable marine resource management and control sea sedimentation; yet, activists believe the new regulation will only ‘further enrich oligarchs’ and ‘increase state income from the fisheries sector’. This is especially true insofar as the potential for food scarcity, as sea sand mining will erode coastal communities’ primary source of sustenance – the sea – while prioritising commercial exploitation and extraction of marine resources.

Addressing the negative impacts of sea sand mining requires a comprehensive approach to sustainable urbanisation, industrial practices, and environmental management. This includes promoting alternative construction materials, implementing stricter regulations on sand extraction, and investing in research and innovation for sustainable infrastructure development. Additionally, it is crucial to raise awareness among policymakers, industry stakeholders, and the public about the environmental consequences of sea sand mining and the importance of adopting environmentally responsible practices.

Image rights: "Sand Extraction at Cliffe Fort" by Shiro Kazan

Export Bans – A Means to Shore-up Ghana in the Bauxite and Iron Ore Industry

Aluminium and Steel remain some of the most widely used materials across industry. Produced from bauxite and iron ore respectively, their demand has led the Ghanian government to establish laws to prohibit the export of bauxite and iron ore in their raw form. The ban is expected to take effect soon and aims to legislate the exploitation, utilisation and management of these resources.

Defending its decision, the government claims that the legislation is “to safeguard the country's limited natural resources and learn from the past mistake of gold exportation”. The origin of the government’s export ban can be traced back to the creation of two statutory corporations, namely:

1. Ghana Integrated Aluminium Development Corporation (GIADEC):

2. Ghana Integrated Iron and Steel Development Corporation (GIISDEC):

A reading of section 28 from GIADEC Act, 2018 and section 30 from GIISDEC Act, 2019 confirms the state’s actions in following procedures for an export ban of bauxite and iron ore respectively. Interestingly, section 4 from both the laws talks about the need to adhere to local content requirements and measures aimed at boosting the country’s upstream and downstream operations. As a result, the Minerals and Mining Local Content and Local Participation Regulations were passed in December 2020 to promote job creation, use of local goods and services, and to improve the attractiveness of domestic businesses in Ghana’s mining sector. These regulations apply to:

holders of mineral rights (holders of reconnaissance and prospecting licences and mining leases);

holders of licences to export or deal in minerals; and

registered mine support service providers

Ghana’s iron ore reserves are estimated at about six billion tonnes and there is potential to start mining operations by 2025. On the other hand, Ghana, the eleventh-largest global producer of bauxite, is also estimated to produce 10 to 20 million tons of bauxite a year from its 900 million tonne reserves. Between 2016 to 2021, production from Ghana decreased by a CAGR of 13.18%. The Ghana Export Promotion Council attributes the decline in production to underutilisation of its reserves and poor infrastructure. Given the absence of bauxite refineries in the country, the mineral is exported to Canada and Scotland for refining and imported from USA and Jamaica to obtain alumina (refined bauxite). It is then processed by the only local smelter in the country, the Volta Aluminium Company Limited (VALCO). Aluworks Ghana, one of VALCO’s major customers further leads the process in aluminium continuous casting and cold rolling mill to produce the raw materials that are used in products ranging from household appliances to aircrafts. As a result, the government has been attempting to fill the vacuum by shoring up VALCO’s production capacity alongside GIADEC’s projects that aim at expanding the country’s exploration and refining capacities. The $1.2 billion deal (2021) to build a bauxite mine and refinery between GIADEC and the Ghanaian-owned Rocksure International showcases the government’s zeal in producing local aluminium products to substitute its annual imports of up to 45,000 tonnes. In addition, Ghana has partnered with China for obtaining the requisite infrastructure and funding to create value-addition to its existing supply chain despite the plausible environmental concerns.

Ghana’s push to limit market access in the bauxite and iron ore industry is similar to Indonesia’s ban on the export of nickel ore for which it is currently facing legal action at the WTO. The rise in such trade restrictive measures also potentially exposes the weaknesses in upholding WTO’s trading principles. Consequently, by promising more jobs, the Ghanaian government must also be wary of the impact of layoffs that such trade-restrictive measures can have on the existing labour engaged in the mining industry. Here, the case study of PT Freeport Indonesia can act as a definite reminder about the ill effects of hasty mining regulations. As far as Ghana’s mining industry is concerned, the export of gold brings maximum revenue to the country. Hence, when introducing new laws to legislate and build its bauxite industry, which amounts to just 0.29% of the global bauxite production, the country’s competitiveness remains to be seen especially when compared to top bauxite producers such as Australia, China or India.

Powering the future: Cobalt in the EV battery value chain

Powering the future: Cobalt in the EV battery value chain

This research paper sheds light on the key risks associated with the supply of cobalt, a critical mineral for the production of electric vehicle (EV) batteries. With demand for EVs projected to grow steadily in the coming decade, it is crucial that companies mitigate these risks. The concentration of finite cobalt reserves in the Democratic Republic of the Congo (DRC) and the concentration of refining capacities in China create a delicate balance of supply that is highly risk prone.

India’s Lithium Rush: Supply Chains, Clean Energy, and Countering China

The discovery of vast lithium deposits in the Indian territory of Jammu and Kashmir is being hailed as a win for the country’s clean energy transition. With the government already promoting domestic EV manufacturing, this could prove to be one of the missing pieces for the puzzle of an Indian EV supply chain.

Background

With rising demand for portable electronics and a push for a low-carbon future, lithium has become one of the most important minerals. Given its application in lithium-ion batteries, it is vital for powering everything from electric vehicles and portable electronics to stationary energy storage systems.

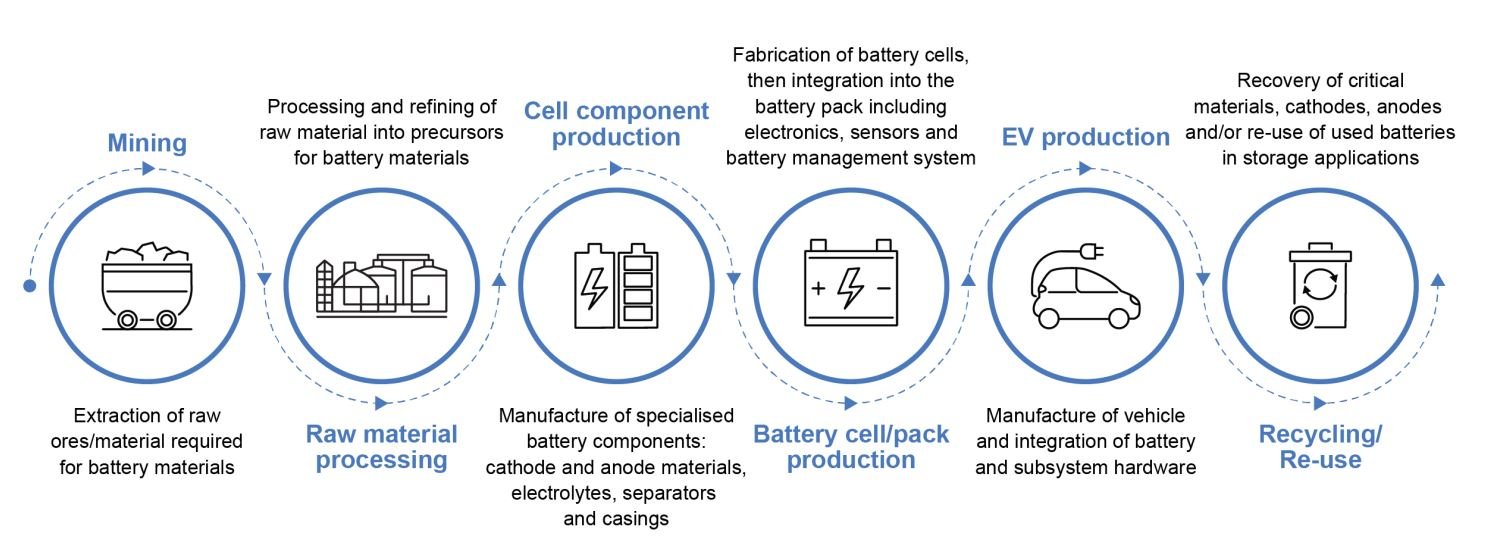

In particular, Lithium-ion battery demand from EVs is set to rise sharply, from the current 269 gigawatt-hours in 2021 to 2.6 terawatt-hours (TWh) per year by 2030 and 4.5 TWh by 2035. According to BloombergNEF’s (BNEF) Economic Transition Scenario (ETS) – which assumes no additional policy measures – global sales of zero-emission cars will rise from 4% of the global market in 2020 to 70% by 2040. Consequently, the global supply chain for lithium has become increasingly important.

EV battery supply chain. Image credit: International Energy Agency

The lithium supply chain is complex, involving multiple stages and players, and is subject to geopolitical and economic factors. Most of the world’s lithium deposits are in the ‘Lithium Triangle’ of the world in South America – Chile, Argentina, and Bolivia. Of these three, however, only Chile Ranks amongst the list of the world’s top lithium producers, headed by Australia. Apart from production, China dominates both the refining and battery manufacturing in the EV battery value chain.

Source: Statista

India: The New Potential Partner of the World

Given the global geopolitical environment, singular dependence on China for a vital resource such as lithium has far-reaching strategic implications. Naturally, democratic nations across the world are prioritizing the reconfiguration of their supply chains for critical manufacturing inputs. Combining its demographic dividend, educated and sufficient workforce, and entrepreneurial spirit– India is rising as a potential and reliable partner. The European Union’s ‘China + 1’ strategy, the EU-India Trade and Technology council, the United States’ recent Initiative for Critical and Emerging Technologies (iCET), and Australia’s Economic Cooperation Trade Agreement with India – testify to the merit that the liberal-democratic world order sees in a partnership with India.

In the given friend-shoring environment that India enjoys, the recent discovery of 5.9 million tons of lithium in the country is monumental. India’s automobile sector itself is transforming. According to NITI Aayog, by 2030, 80% of two and three-wheelers, 40% of buses, and 30 to 70% of cars in India will be EVs. The newly found lithium can help the nation meet rising demand, both domestically and globally. India’s government has already been pushing for electric mobility and domestic EV manufacturing. The 2023-24 Union Budget, allocated INR 35,000 crore for crucial capital investments aimed at achieving energy transition, including efforts for electrification of at least 30% of the country's vehicle fleet by 2030 and net-zero targets by 2070. For EV manufacturers, the government has launched initiatives such as the Faster Adoption of Manufacturing of Electric Vehicles Scheme – II (FAME – II), allocating approximately $631 million towards subsidizing and promoting the adoption of clean energy vehicles.

Indian Lithium deposits: Risks and Challenges

The recent discovery in the Reasi district of the Union territory of Jammu and Kashmir solves one of the major challenges to a localized li-ion battery supply chain in the country– access to lithium deposits. However, there are more challenges ahead.

Firstly, the Reasi district is just 100 kilometres from the Rajouri district, a geopolitically sensitive area. Although today these areas are well-connected to India with proper infrastructure, including airports and highways, the Line of Control between India and Pakistan is less than 100 kilometres from Rajouri and around 200 kilometres from Reasi. The region’s proximity to Azad Jammu and Kashmir also makes it vulnerable to militant activities. Greater infrastructural development in the region, including a robust logistics network will have to be developed to ensure an uninterrupted indigenous supply chain (given that other stages of the supply chain are also established domestically).

Secondly, although the Geological Survey of India (GSI) has the capacity to discover and locate lithium deposits, the remainder of the value chain to produce commercial-grade lithium indigenously is not in place. Similar to Australia, Canada, and China, the identified lithium reserves in India are in hard rock formations. In order to extract the resource, mining capabilities will first have to be established in the region. It is still unclear whether these reserves will be managed by state authorities or undertaken by the central government, given the strategic importance of the resource. Furthermore, whether the mines be auctioned, like India’scoal mines, or entrusted to a public sector enterprise, is not yet known.

Timely and major investment in developing refining, processing, and purification technologies will be required. India will have to build a large-scale capacity for transforming extracted material into high-purity lithium in order to take full advantage of this discovery. While the opportunity is considerable, so are the costs. India’s government will need to devise a clear strategy that effectively helps both the country’s energy transition and domestic manufacturing ambitions.

Image credit: Nitin Kirloskar via Flickr

Powering the future: Lithium in the EV battery value chain

Powering the future: Lithium in

the EV battery value chain

This research paper is the first in a series covering the numerous risks associated with electric vehicle (EV) battery production. Each paper delves into a specific mineral that is vital to this process, starting off with lithium. This series is brought by a team of analysts from the Global Commodities Watch.

Red metals reach the red: Peruvian protests impact the global copper supply

As the world gears up to mitigate the far-reaching effects of climate change—many of which are already being felt—investment into zero-emission technologies is growing to complement more than 70 countries’ mid-century net-zero emission targets. Copper will be a key component to energy-efficient technologies, including electric vehicles, charging infrastructure, solar PV, wind, and batteries. For this reason, copper demand is projected to double over the next 10 years and more than triple by 2050; but this may have detrimental social, political, and economic impacts on the surrounding contexts of copper mines, which may, in turn, have repercussions on the global supply and cost of copper.

Peru, for instance, holds the world’s second largest reserve of copper, which contributes to 4% of Peru’s entire GDP; however, local communities that live around the Apurímac-Cusco-Arequipa Road mining corridor continue to be the poorest in Peru. The mining industry has foregone environmental and health restrictions, while increasing inequality in mining districts, thus contributing to existing socioeconomic tensions among local Peruvian communities, for instance against the Antapaccay mine in Espinar, the Las Bambas mine in Cotabambas, and the Cuajone mine in Moquegua. Such enmities have been exacerbated in the ongoing political crisis in Peru that began in December 2022.

The past five decades in Peru were foundational to the country’s current political crisis. Insurgency during the 1970s, multiple dictatorships, and resulting economic instability generated political and social strife, which collectively exploded upon President Castillo’s impeachment after he attempted to install an emergency government and rule by decree in December 2022.

Castillo is highly supported by Peru’s rural populations, many of whom live in the surrounding areas of copper mines, as he denounced foreign mining corporations and their negligence of environmental regulations, promised higher taxes and wealth redistribution policies, safer working conditions for miners, and nationalisation of the entire mining industry.

After Castillo’s removal, political tensions among local miner communities—as well as much of Peru’s left-wing population—rose, leading to worker strikes, protests against mines, and disruption of mining operations. This includes ceasing operations at the Las Bambas mine, which alone supplies 2% the world’s copper. The Antapaccay mine stopped production in mid-January, but has since resumed. Continued nationwide protests threaten to cut access to $4 billion worth of red metal, including copper. In 2022, growth potential of mining GDP from 2.9% to 0.3%, due to social unrest.

To re-establish the export of copper from Peru, mining companies such as Glencore, MMG Limited, and Freeport-McMoRan must enter into agreements with local communities, in conjunction with the newly formed government led by Dina Boluarte. The mining industry should address grievances in a manner that reduces poverty, prevents environmental and health impacts, and allows for inclusive employment of the surrounding communities.